Navigating Personal Finance, Tech Skills, and Real Estate: Your 2026 Guide to Building Wealth in America

Hi Friends – whether you're a fresh-faced Gen Z'er just starting your first job or a seasoned pro eyeing that next big move, let's talk money. Back in the day, financial security meant punching the clock at the same gig for decades, socking away a bit in savings, and snagging a cozy house with a white picket fence. But in 2026, with inflation still nibbling at our wallets (hovering around 2.7% lately), skyrocketing home prices in hotspots like Miami and Orlando, and tech flipping industries upside down overnight, that old playbook just doesn't cut it anymore. We're all rethinking how we hustle, stash, and grow our cash.

From young folks juggling student loans and gig work to mid-career types plotting an early exit from the grind, the focus is on smart, sustainable strategies. Personal finance isn't about pinching every penny – it's about building a system that works for you long-term. Tech skills? They're your ticket to bigger paychecks and remote freedom. And real estate? It's evolved from just owning your home to creating real assets that pay you back. The U.S. gives us killer opportunities with our massive stock market, booming tech scene (hello, AI everything), and diverse property landscape. But yeah, it can bite if you're not prepared – think hidden fees, market dips, or bad zoning surprises.

This isn't some stuffy textbook; it's your no-BS roadmap to stacking wealth in today's America. We'll break it down simply, with real steps you can take right now. Picture it as chatting with a savvy friend over coffee, connecting the dots between managing your money, leveling up your skills, and dipping into real estate. Ready to redefine your financial game? Let's dive in.

Mastering Personal Finance and Investing in America

Demystifying the U.S. Stock Market: It's Not as Scary as It Sounds

Listen, the U.S. stock market isn't some Vegas crapshoot – it's where millions of us build real wealth, even if we're not day-trading pros. If you've got a 401(k), IRA, or even a basic brokerage account like those on Fidelity or Robinhood, you're probably already in the game. At its heart, stocks let you snag a piece of actual companies. Buy shares in something like Apple or Amazon, and you're basically a mini-owner. As they grow – cranking out profits from iPhones or cloud services – your slice grows too.

What sets our market apart? It's huge, with the NYSE and NASDAQ hosting giants backed by tough rules on transparency and reporting. No shady dealings here; everything's out in the open. Sure, we've seen rough patches – think the 2008 crash or 2022's inflation hit – but history shows patient investors win big over time. The S&P 500, a key benchmark, has averaged about 10% annual returns long-term. In 2026, experts are optimistic: Goldman Sachs predicts sturdy 2.6% U.S. GDP growth, outpacing global averages, thanks to tax cuts and easing tariffs. AI stocks are still hot, with Wall Street eyeing an 11% S&P climb.

Rookie mistake? Chasing TikTok hype stocks without digging into the business. Skip that – go for index funds or ETFs that track the whole market, or dividend payers that spit out steady cash. They're like the reliable pickup truck of investing: lower drama, solid gains.

Stock Market Trends Every American Investor Should Track in 2026

Markets don't move in a vacuum – they're tied to Fed moves, jobs numbers, inflation, and even global drama. The Federal Reserve's still king: Rate hikes make borrowing pricier, cooling growth and shifting folks from flashy tech stocks to stable value plays. But with rates potentially dipping below 4% by mid-2026, borrowing could ease up, boosting valuations.

Retail investing's exploding too, thanks to apps like Robinhood and Fidelity making it dead simple (and often free) to jump in. Over 20 million new accounts popped up last year alone. It's empowering, but watch for impulse trades – pros stick to long-haul plans over daily swings. ESG's huge now: More of us want investments matching our values, like green energy or ethical firms. In 2026, watch for AI's continued boom (think Nvidia's gains), but analysts warn of risks if earnings don't match hype. Broader growth from sectors like consumer goods and industrials could shine, especially with the One Big Beautiful Act cutting corporate taxes by $129 billion through 2027.

Stay informed without obsessing: Check apps weekly, diversify, and remember – time in the market beats timing the market.

Smart Budgeting Tips for Gen Z and Millennials Facing U.S. Realities

Budgeting sounds like a drag, right? Like giving up your daily latte. But trust me, it's your secret weapon for freedom – especially with rents up 5% in cities like NYC and student debt averaging $37k. For younger Americans, it's about gaining control amid chaos: 73% feel paycheck-to-paycheck, per recent surveys, but 59% are savvy about saving in one spot to splurge elsewhere.

Start with the classic 50/30/20: Half your after-tax income on needs (rent, groceries), 30% on wants (streaming, outings), 20% on savings/debt. In pricey spots like LA or Seattle, tweak it – maybe 60/25/15. Apps make it painless: Mint, YNAB (You Need A Budget), Empower. Loud budgeting's trending too – owning your limits publicly, like "I'm skipping brunch to build my emergency fund." Surveys show 44% aim to save more in 2026, 36% to crush debt, and 30% to cut spending. Focus on short-term wins: Build that three-month safety net first. Track habits, adjust monthly, and celebrate progress – it's about building momentum, not perfection.

Is Early Retirement Realistic in America? The FIRE Movement Says Yes

Dreaming of ditching the 9-to-5 by 50? It's not pie-in-the-sky anymore. The FIRE (Financial Independence, Retire Early) crowd proves it: Save aggressively (40-60% of income), invest smartly, and you're golden. Gen Z eyes retiring at 54, Millennials at 60 – way ahead of Boomers' 71.

Key? Low-cost index funds, dividend stocks, and passive income like rentals. But plan for U.S. quirks: Healthcare's a beast – Medicare kicks in at 65, so bridge that gap with HSAs or private plans. The 4% rule's evolved; creator Bill Bengen now says 4.7% safe withdrawal for 30 years, even higher in low-inflation times. Many "retirees" pivot to consulting or hobbies that pay. It's about choice, not lounging forever. With 37% seeing retirement age as "financial happiness," start small: Max your Roth IRA ($7,500 limit in 2026), automate savings, and track net worth. Discipline pays off – think compounding turning $5k yearly into millions over decades.

Leveling Up with SaaS and Software Skills for U.S. Career Growth

Why SaaS Skills Are a Game-Changer in America's Economy

SaaS (Software as a Service) isn't just buzz – it's the engine running U.S. businesses from startups to Fortune 500s. Think cloud tools handling sales, HR, finance – all updated automatically, accessible anywhere. In 2026, the market's exploding to $315 billion, with AI supercharging everything.

Employers crave folks who master these: Learn quick, automate drudgery, boost efficiency. It means fatter paychecks (up 20% often), job security, and remote gigs. With AI-native teams rising, skills in tools like HubSpot or Zoho aren't optional – they're your edge in a tech-driven economy.

Getting Started with Salesforce: A Beginner's Power Move

Salesforce dominates CRM in the U.S., tracking leads, customers, and sales for giants like Coca-Cola. It looks intimidating, but basics are straightforward: Objects like accounts and opportunities organize data for real-time insights.

Why learn? High-demand jobs – admins average $95k, consultants $120k+. In 2026, with 9.3 million ecosystem jobs projected, add AI (Einstein) and integrations for a boost. Free Trailhead trails make it fun; certify as a beginner and doors open wide.

AI Automation: Scaling Your U.S. Business Like a Pro

AI's revolutionizing entrepreneurship – tools like Zapier or Make automate emails, data entry, reports. For solopreneurs, it's gold: One person runs what used to need a team, cutting costs 30-50%.

In 2026, agentic AI (smart decision-makers) hits mainstream, per PwC. Build workflows connecting apps – think auto-follow-ups or inventory alerts. Ethical use is key; start small with free tiers, scale as you grow. It's your competitive moat.

Video Editing Tools: Boosting Your Content and Marketing Game

Video rules U.S. digital – YouTube, TikTok, ads. Pros use Adobe Premiere Pro, DaVinci Resolve (free!), or Final Cut Pro for Mac speed.

Not a creator? Businesses need video for training, stories. Skills open freelance doors ($50/hr+). Add AI like in CapCut for auto-edits. It's engaging audiences, simplified.

Diving into U.S. Real Estate Investing

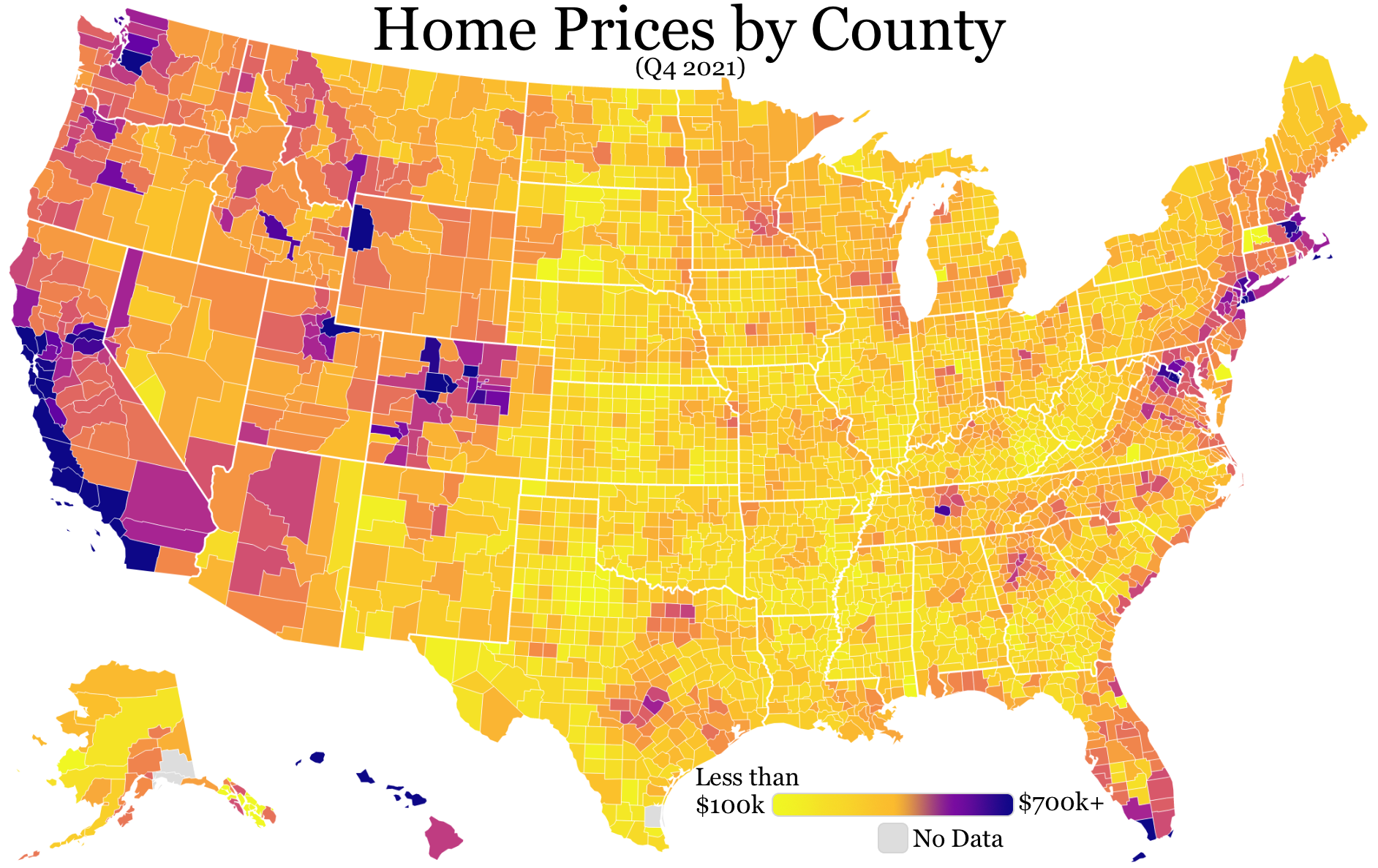

The Real Scoop on How America's Real Estate Market Operates

U.S. real estate's no monolith – it's hyper-local. Coastal spots like Cali chase appreciation; Midwest focuses on cash flow from steady rents. Job growth, migration (South's booming), rates (hovering 6.3% avg in 2026), and regs drive it.

In 2026, expect a "great reset": Sales up 3% to 4.2M, prices +1-2%, more inventory (up 9%). Research local data on sites like Zillow or Realtor.com over headlines for wins.

REITs Demystified: Easy Entry for New Investors

No cash for a whole building? REITs let you invest in portfolios – apartments, malls, data centers – without management hassles. They trade like stocks on exchanges like Vanguard's VNQ ETF, must pay 90% profits as dividends.

Great for beginners: Passive income, diversification, IRA-friendly. Top picks for 2026: Prologis (industrial, 2.9% yield), Realty Income (retail, "monthly dividend company"). Aim for 10-15% returns; start with ETFs like VNQ.

Snagging Your First U.S. Rental Property: Step-by-Step

Ready for hands-on? Rentals build equity and income. Finance via FHA loans (3.5% down for owner-occupiers) or conventional loans (20% down).

Pick wisely: Analyze location (job hubs), cash flow (rent covers mortgage+), management (DIY or pros like AppFolio?). Understanding tax advantages such as depreciation (deduct building value over 27.5 years), mortgage interest write-offs, and 1031 exchanges is huge. In 2026, bonus depreciation at 100% lets you accelerate deductions on improvements via cost segregation – slashing taxes big-time. Budget for surprises (repairs 1-2% value yearly), screen tenants, and scale slowly. It's work, but passive wealth awaits.

#PersonalFinance #RealEstateInvesting #SaaSSkills #WealthBuilding2026 #USEconomy #EarlyRetirement #StockMarketTips #FinancialIndependence

USA Personal Loan Calculator

Monthly Payment: $0

Total Payment: $0

Total Interest: $0

No comments:

Post a Comment